𝐃𝐢𝐬𝐜𝐥𝐨𝐬𝐮𝐫𝐞, 𝐒𝐮𝐛𝐬𝐢𝐝𝐢𝐚𝐫𝐲 𝐓𝐫𝐚𝐧𝐬𝐩𝐚𝐫𝐞𝐧𝐜𝐲 𝐚𝐧𝐝 𝐭𝐡𝐞 𝐑𝐚𝐣𝐞𝐬𝐡 𝐄𝐱𝐩𝐨𝐫𝐭𝐬 𝐂𝐚𝐬𝐞

The recent developments involving Rajesh Exports have brought renewed focus to an important question in securities regulation: 𝘸𝘩𝘦𝘯 𝘥𝘰𝘦𝘴 𝘢 𝘥𝘪𝘴𝘤𝘭𝘰𝘴𝘶𝘳𝘦 𝘪𝘯𝘤𝘰𝘯𝘴𝘪𝘴𝘵𝘦𝘯𝘤𝘺 𝘣𝘦𝘤𝘰𝘮𝘦 𝘦𝘷𝘪𝘥𝘦𝘯𝘤𝘦 𝘰𝘧 𝘮𝘪𝘴𝘳𝘦𝘱𝘳𝘦𝘴𝘦𝘯𝘵𝘢𝘵𝘪𝘰𝘯, 𝘢𝘯𝘥 𝘸𝘩𝘦𝘯 𝘥𝘰𝘦𝘴 𝘪𝘵 𝘮𝘦𝘳𝘦𝘭𝘺 𝘸𝘢𝘳𝘳𝘢𝘯𝘵 𝘧𝘶𝘳𝘵𝘩𝘦𝘳 𝘦𝘹𝘱𝘭𝘢𝘯𝘢𝘵𝘪𝘰𝘯?

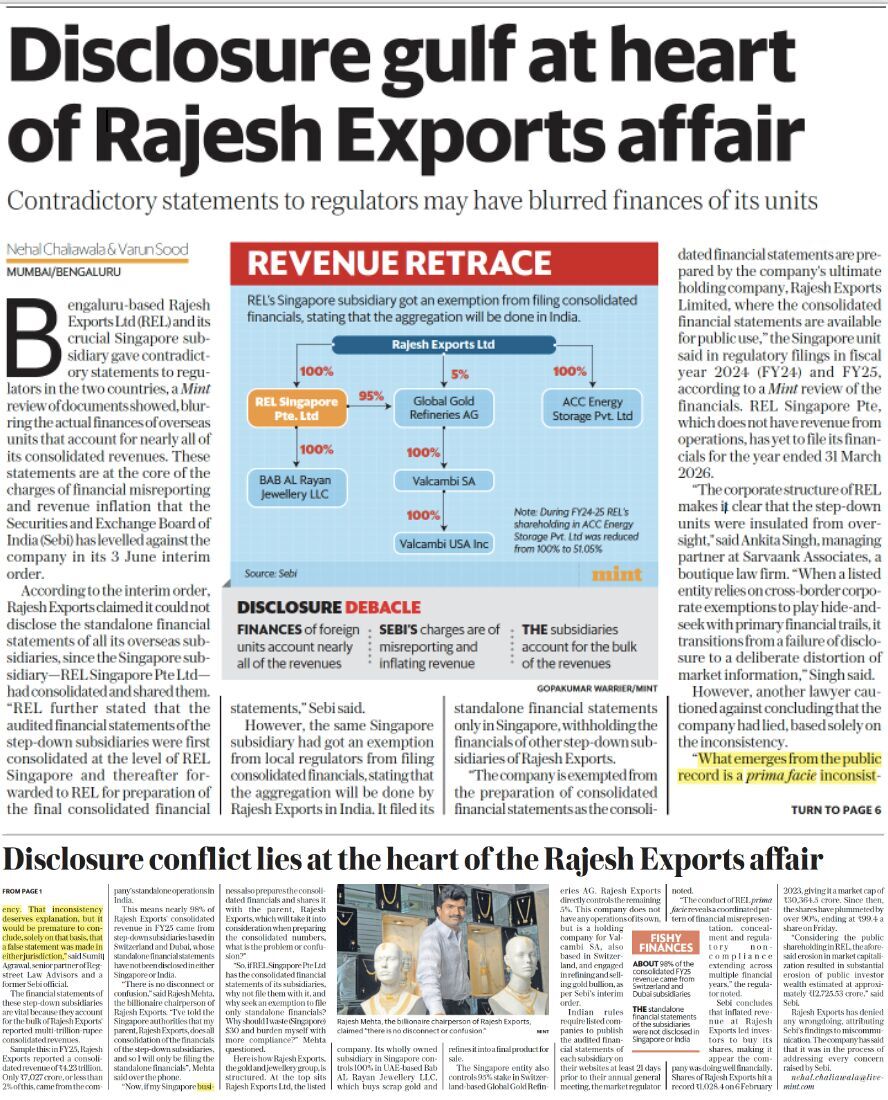

A Mint article titled “Disclosure gulf at heart of Rajesh Exports affair” examines the apparent inconsistency between statements made by Rajesh Exports and its Singapore subsidiary regarding the preparation and disclosure of financial statements of overseas subsidiaries that account for a substantial portion of the group’s reported revenues.

In this context, Mr. Sumit Agrawal, Senior Partner at Regstreet Law Advisors and former SEBI officer, offered an important perspective on the issue:

“𝘞𝘩𝘢𝘵 𝘦𝘮𝘦𝘳𝘨𝘦𝘴 𝘧𝘳𝘰𝘮 𝘵𝘩𝘦 𝘱𝘶𝘣𝘭𝘪𝘤 𝘳𝘦𝘤𝘰𝘳𝘥 𝘪𝘴 𝘢 𝘱𝘳𝘪𝘮𝘢 𝘧𝘢𝘤𝘪𝘦 𝘪𝘯𝘤𝘰𝘯𝘴𝘪𝘴𝘵𝘦𝘯𝘤𝘺. 𝘛𝘩𝘢𝘵 𝘪𝘯𝘤𝘰𝘯𝘴𝘪𝘴𝘵𝘦𝘯𝘤𝘺 𝘥𝘦𝘴𝘦𝘳𝘷𝘦𝘴 𝘦𝘹𝘱𝘭𝘢𝘯𝘢𝘵𝘪𝘰𝘯, 𝘣𝘶𝘵 𝘪𝘵 𝘸𝘰𝘶𝘭𝘥 𝘣𝘦 𝘱𝘳𝘦𝘮𝘢𝘵𝘶𝘳𝘦 𝘵𝘰 𝘤𝘰𝘯𝘤𝘭𝘶𝘥𝘦, 𝘴𝘰𝘭𝘦𝘭𝘺 𝘰𝘯 𝘵𝘩𝘢𝘵 𝘣𝘢𝘴𝘪𝘴, 𝘵𝘩𝘢𝘵 𝘢 𝘧𝘢𝘭𝘴𝘦 𝘴𝘵𝘢𝘵𝘦𝘮𝘦𝘯𝘵 𝘸𝘢𝘴 𝘮𝘢𝘥𝘦 𝘪𝘯 𝘦𝘪𝘵𝘩𝘦𝘳 𝘫𝘶𝘳𝘪𝘴𝘥𝘪𝘤𝘵𝘪𝘰𝘯.”

The observation highlights a key regulatory principle. While inconsistencies in disclosures may legitimately raise questions and warrant scrutiny, the existence of conflicting statements alone may not be sufficient to establish fraud, misrepresentation or regulatory violations without a deeper examination of the underlying facts, reporting framework and disclosure obligations across jurisdictions.

The matter also underscores broader governance considerations relating to transparency of overseas subsidiaries, availability of subsidiary financial information to investors, and the challenges of regulatory oversight in complex cross-border corporate structures.

As regulatory proceedings continue, the case is likely to contribute to ongoing discussions around disclosure standards, investor protection and accountability in multinational corporate groups.

Link to article: https://lnkd.in/ggiHbYzn

Can disclosure inconsistencies, by themselves, justify an inference of misrepresentation, or should regulators first establish a clearer evidentiary foundation? Readers may share their views on info@regstreetlaw.com