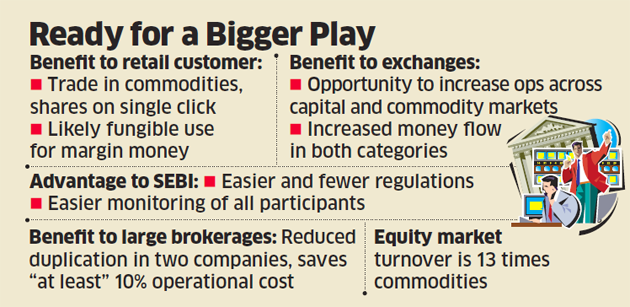

Mumbai: The Securities and Exchange Board of India (Sebi) has made it easier for retail investors to move their money between shares and commodities, like gold and oil.

The regulator last week issued an amendment to regulations that concern brokers and sub-brokers, allowing anyone registered to trade in shares to also trade in commodities, and vice versa, without cumbersome paperwork, a second verification process, and through an alternate account.

“In the future, if a customer wants to switch asset classes, it can be done on a single click without irritants of paperwork that may earlier have pushed the customer to stick to just a single asset class,” said Lalit Thakkar, director at Angel Broking.

Large broking houses like Angel Broking, Edelweiss and Motilal Oswal have separate subsidiaries that trade in commodities. Each time an investor wants to move from shares to commodities, cheques and permissions to move money from one unit to another are required.

For such firms, the effort and cost of supporting two organisations will decline, but for the retail customer the advice wouldn’t change. Amit Rathi, director, Anand Rathi Commodities, a subsidiary of Anand Rathi Financial Services, estimates expenses being cut by “at least” 10%. But for smaller brokers that practice solely in equities or commodities this could be a game changer.

The move is a precursor to a unified market licence for trading in any financial instrument market, where an equity exchange like NSE or BSE will be able to offer a platform for trading commodity futures and a commodity exchange like MCX or NCDEX will be able to offer equities trading.

Sebi still has to spell out the operational rules on a unified broker’s licence, but market participants are optimistic the move will lead to an increase in turnover of both the equity and commodity derivatives markets. Crosseas Capital managing director Rajesh Baheti is of the same view. “At the moment, a trader loses a day in moving money from one arm to another if he has to change asset classes from shares to commodities,” he said.

Crosseas Capital is among the leading proprietary traders on the National Stock Exchange. The combined turnover — demat cash and derivatives — of NSE and BSE was Rs 709.46 lakh crore in the fiscal year to December 2016, up 31% from the year earlier. In the same period, the turnover of the metals and energy bourse MCX, agri bourse NCDEX and plantations exchange NMCE grew 2% to Rs 51.15 lakh crore, Sebi statistics show.

“It will help Sebi in better monitoring the settlement and risk-management mechanism,” said Sumit Agrawal, partner, Suvan Law Advisors. “While the nitty gritty on margins, stamp duty, taxation etc. would require to be specified, this move will create a new era of better regulation and ease of doing business for investors.”

His comment takes on board the margin money that each investor must deposit before making trades. At the moment, margin money deposited for either asset class is different and so is taxation, which depends on sales and reinvestment.

Unlike the equity market, which has a cash as well as a derivatives segment, the commodity market only offers derivatives trading because the spot market in commodities is regulated by individual state governments. Turnover in equity derivatives is significantly higher than the commodity counterpart.

Another benefit of the unified licence is that traders can easily switch over to the commodity segment after the stock exchanges close at 3:30 pm. The commodity exchanges run from 10 am to 11:30 pm.

The ministry of finance, Sebi and Reserve Bank of India jointly regulate capital markets. The Forward Markets Commission, which regulates commodity futures, was absorbed by Sebi in September 2015 for better regulation in the wake of the NSEL commodity market scam.

One of the major benefits of combining arms for large broking firms is operational efficiency. Equity firms are already beginning to consider it. “We’ll have to see… whether to merge the two arms or for the equity arm to buy out the commodity arm and save on expenses,” said Prashant Bhansali, director, Mehta Equities.